Asymmetric and symmetric meta-correlations in financial markets

Li Xiaohui, Shen Xiangying, Huang Jiping†,

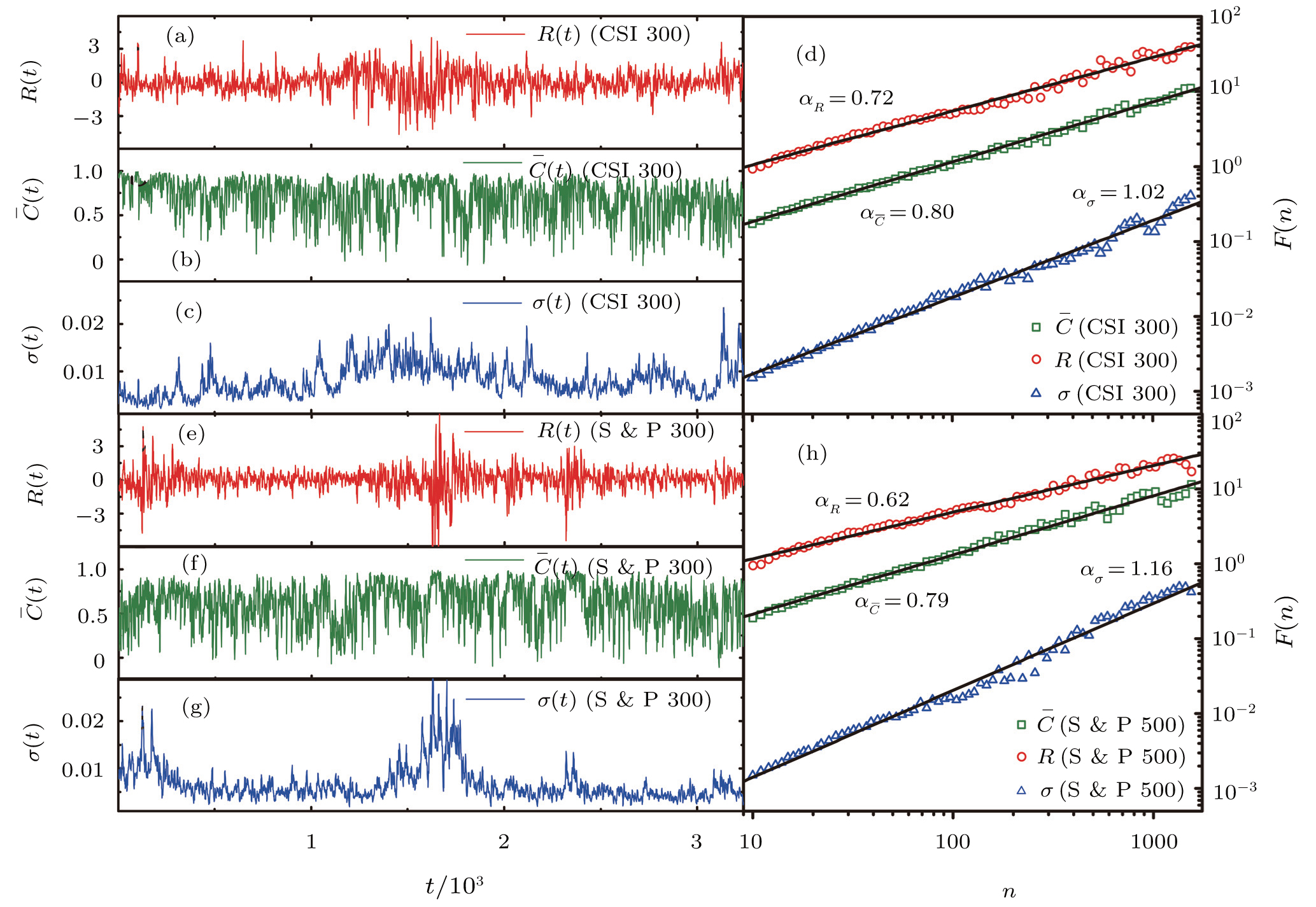

Three time series for CSI 300, normalized index return

Asymmetric and symmetric meta-correlations in financial markets |

|

Li Xiaohui, Shen Xiangying, Huang Jiping†,

|

Three time series for CSI 300, normalized index return |

| |